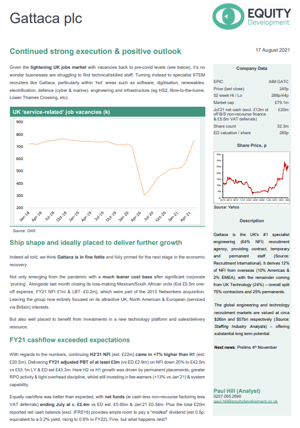

Given the tightening UK jobs market with vacancies back to pre-covid levels, it’s no wonder businesses are struggling to find technical/skilled staff. Turning instead to specialist STEM recruiters like Gattaca, particularly within ‘hot’ areas such as software, digitisation, renewables, electrification, defence (cyber & marine), engineering and infrastructure (eg HS2, fibre-to-the-home, Lower Thames Crossing, etc).

Gattaca has updated today that in the 12 months to end July continuing H2’21 NFI was 7% higher than H1. Delivering FY21 adjusted PBT of at least £3m (vs ED est. £2.9m) on NFI down 20% to £42.5m vs £53.1m. Cashflow was also better than expected, with net funds (ie cash less non-recourse factoring less VAT deferrals) ending July at c. £2.4m vs ED est. £0.65m.

We think the group is in fine fettle and fully primed for the next stage in the economic recovery, emerging from the pandemic with a much leaner cost base after significant corporate ‘pruning’. Plus the total £20m reported net cash balance (excl. IFRS16) provides ample room to pay a “modest” dividend.

At this stage, we have conservatively held our FY22 forecasts, but nudged up our fair value to 285p/share from 280p thanks to the favourable outlook & July cash out-turn.